Direct Answer: Most Washington dental plans cover preventive care at or near 100%, basic restorative work at 70-80%, and major procedures at around 50%, with an annual payout cap that runs out faster than most patients expect.

Before mentioning what kind of appointment they need, a meaningful number of people who contact our office open with some version of the same question: do you take my insurance? We see it in form submissions, we hear it in the first few seconds of phone calls, and we understand why. For most adults in Renton and across South King County, confirming coverage is the prerequisite, not the formality.

What surprises a lot of those same people is how much they don’t know about the plan they’re depending on. They know they have Delta Dental, or a plan through their employer, or something through the Washington State PEBB program. But the details, the tier structure, the annual cap, what counts as “major” care, often only surface mid-treatment, when the number is already on the table.

This article isn’t about a specific plan or a specific practice. It’s about how Washington dental insurance actually works, where the gaps are, and what to look for before you’re sitting in the chair wondering why your estimate is higher than you expected.

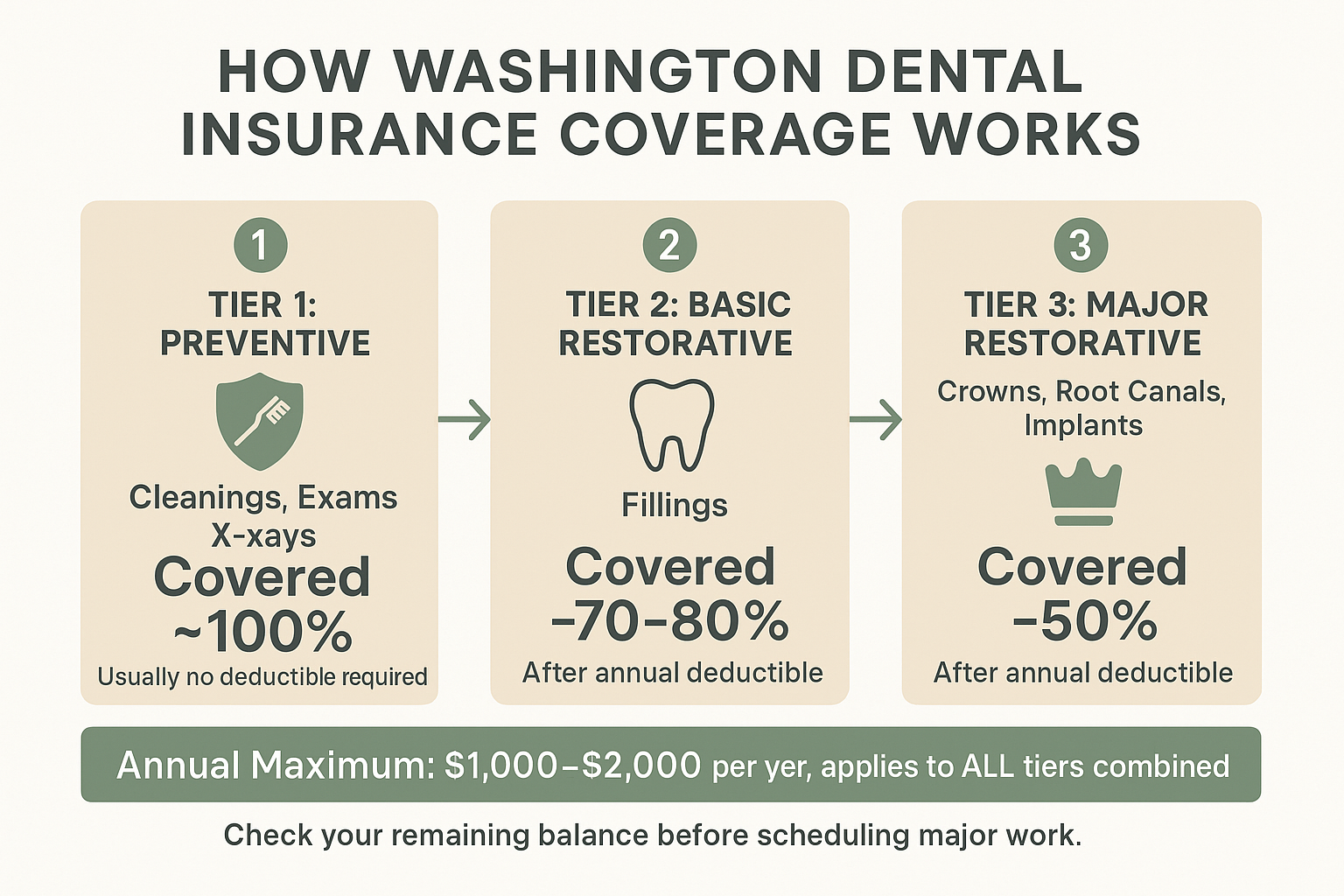

The Three-Tier Structure Most Washington Plans Use

The majority of commercial dental plans in Washington, whether through an employer, the PEBB marketplace, or a standalone policy, organize benefits into three tiers. Understanding those tiers is the single most useful thing you can do before scheduling any restorative work.

Tier 1: Preventive care. This includes routine cleanings, exams, and X-rays. Most plans cover these at or near 100%, which is why they’re sometimes called “free” visits. They’re not free, they’re the benefit your premium is designed to fund.

Tier 2: Basic restorative care. Fillings fall here. Most plans cover basic restorative work at 70-80% after your deductible. So on a $200 filling, you’d typically owe somewhere in the $40-60 range, depending on your specific plan terms.

Tier 3: Major restorative care. This is where patients run into the biggest surprises. Crowns, root canals, and implants almost always fall into this category, and most plans cover them at 50%. That means on a procedure that might cost $1,200-1,800 in the Renton area, your plan could cover $600-900, and you’d be responsible for the rest, out of pocket, after your deductible.

The reason this matters: a patient who books a cleaning, then learns at that appointment that they also need a crown, may walk into the estimate conversation without knowing their crown will be classified as “major” care. That’s not a billing surprise, it’s a coverage structure most people have never been shown clearly. Reading your plan’s Summary of Benefits before you schedule major work takes about ten minutes and can prevent a lot of confusion.

Annual Maximums: The Number Most Patients Don’t Think About Until It Matters

Nearly every dental plan in Washington sets an annual maximum, the most the plan will pay out in a single benefit year, across everything. That number resets every January 1st (or on your plan anniversary, depending on how it’s structured).

For most commercial plans, that cap sits somewhere in the $1,000-2,000 range per year. It sounds reasonable until you start doing the math. A cleaning, a set of bitewing X-rays, one filling, and one crown can collectively push your plan to its limit, or past it, in a single calendar year. And every dollar over that ceiling is yours to cover.

Here’s the practical advice: if you’ve already had your cleaning and a filling or two this year, call your insurance company or log into your member portal and ask how much of your annual maximum has already been used. Most plans make this visible online. Knowing your remaining benefit before you schedule a crown tells you exactly what your financial exposure will be, and whether it makes sense to try to schedule that crown before December 31st, when benefits reset and you’d be spending against a fresh maximum.

The deductible piece matters here too. If you’ve already met your annual deductible, often $50-100 on most Washington plans, then any additional work you schedule before year-end doesn’t require you to meet it again. Scheduling a needed crown in November rather than waiting until February means you’re working with a deductible that’s already satisfied.

A Quick Look at How Washington Dental Plan Coverage Stacks Up

This breakdown shows how the three coverage tiers typically apply, and where the annual maximum starts to compress your benefits.

FSAs and HSAs: Tax-Free Money That Works for Dental Care

If you have a Flexible Spending Account (FSA) or Health Savings Account (HSA) through your employer, that money can be used for dental care, including crowns, implants, periodontal treatment, and other procedures your insurance might only partially cover.

An FSA is a pre-tax account funded by payroll deductions. The money goes in before taxes are calculated, which means you’re effectively paying for dental care with a discount equal to your tax rate. For 2026, the Health Care FSA contribution limit is $3,400 per employee.

The catch with FSAs is the use-it-or-lose-it rule. If you’re a Washington State employee covered under the PEBB program, you can carry over up to $680 of unused FSA funds into the following year, but anything above that amount is forfeited. The Washington State Health Care Authority confirms this carryover limit and the forfeiture rule for PEBB participants.

In practical terms: if you’re in the second half of the year and you have $800-1,500 sitting in an FSA, and you’ve been putting off a crown or periodontal work, this is the most useful time to schedule it. The money is already earmarked. Using it on dental care is exactly what it’s designed for.

HSAs work a bit differently, they roll over indefinitely, there’s no forfeiture deadline, and the funds can even grow tax-free if invested. If you have an HSA and a high-deductible health plan, dental expenses qualify, and using HSA funds for a crown or implant procedure is a straightforward way to reduce what you actually pay out of pocket.

FSA vs. HSA: Key Differences for Dental Patients

Both account types can pay for dental care, but the rules are different. Here’s a side-by-side comparison of what matters most.

| Feature | Health Care FSA | HSA |

|---|---|---|

| 2026 Contribution Limit | $3,400 per employee | $4,300 individual / $8,550 family |

| Rollover Rule | Up to $680 (PEBB), rest is forfeited | Full rollover, no deadline |

| Eligibility Requirement | Employer must offer it | Must have a qualifying high-deductible health plan |

| Can Cover Dental Care? | Yes | Yes |

| Best Used For | Planned work in the current benefit year | Ongoing or future dental expenses at any time |

| Year-End Urgency? | Yes, schedule before December 31 | No, funds carry forward indefinitely |

The Senior Coverage Gap: What Medicare Actually Does (and Doesn’t) Cover

This is one of the most misunderstood areas of dental coverage in the South King County area, and it affects a lot of adults who have otherwise good healthcare coverage.

Medicare Part A and Part B do not cover routine dental care. That means cleanings, fillings, crowns, and root canals are not included, not as a hidden benefit, not with a referral. Medicare was not designed to cover dental, and for most enrollees, it still doesn’t.

Some Medicare Advantage plans (Part C) do include limited dental benefits, but coverage varies widely by carrier and plan. Some cover only preventive care. Others include a small allowance for major work. A few are more generous. The only way to know what your specific plan covers is to read the Summary of Benefits or call the plan directly.

For adults 65 and older in Renton, Tukwila, Kent, and Burien, this gap typically means one of three paths:

- Purchasing a standalone dental plan, which often has its own waiting periods and annual maximums

- Enrolling in a Medicare Advantage plan that includes dental, with careful attention to what’s actually covered

- Paying out of pocket for some or all dental work, particularly for crowns and periodontal procedures

If you’re in or approaching Medicare age and haven’t confirmed what dental coverage you actually have, a quick call to your plan’s member services line is worth fifteen minutes. The answer directly affects how you plan and sequence any major dental work, including procedures like bone grafting or implants that require multiple appointments and significant investment.

The Missing Tooth Clause: A Surprise Many Patients Don’t See Coming

If you lost a tooth before your current dental coverage began, there’s a good chance your plan won’t pay to replace it. This is called the missing tooth clause (sometimes listed as a “pre-existing condition” limitation in dental plan language), and it’s one of the most common painful surprises in restorative dentistry.

Here’s how it works: a patient loses a tooth a few years ago, doesn’t have insurance at the time, then gets coverage through a new employer. They assume the implant they’ve been putting off is now partially covered. They come in, the plan of care is explained, and then, when they call their insurance to verify, they learn the plan excludes teeth that were missing before the coverage start date.

This clause isn’t buried in fine print to deceive anyone. It’s standard in many commercial plans, but most people never read the limitations section of their policy.

Before scheduling any implant or bridge work for a tooth you lost more than a few months ago, open your plan’s Limitations and Exclusions section, usually a few pages into the Summary of Benefits, and search specifically for language about “missing teeth” or “pre-existing tooth loss.” If the language is unclear, a quick call to your insurance company’s member services line can tell you directly whether your specific situation is excluded.

If you’re weighing your options after tooth loss, this article on when a dental implant is the right choice after tooth loss walks through the clinical decision, separate from the insurance question.

Frequently Asked Questions About Dental Insurance in Washington

Does Cedar Dental Group accept my insurance?

The best way to confirm is to call us directly at 425-430-0400 with your insurance card in hand. Our front desk can verify your plan and let you know what’s covered before you come in. We know insurance confirmation is the first question most new patients have, and we’d rather answer it clearly before you schedule than have you discover a mismatch at the appointment.

What does ‘in-network’ versus ‘out-of-network’ actually mean for what I pay?

When a dental practice is in-network with your plan, the provider has agreed to accept the plan’s fee schedule. That means your cost-share (the 20-50% you owe after insurance pays) is calculated against a pre-negotiated rate, which is usually lower than the practice’s standard fee. Out-of-network means the practice hasn’t signed that agreement, so your insurance may pay less, and the gap between what insurance covers and what the practice charges falls to you. Always ask your insurance company for both in-network and out-of-network benefit rates before scheduling major work.

My deductible is already met for the year. Should I schedule restorative work before December 31st?

Generally, yes, if you need the work and your annual maximum hasn’t been fully used. Once your deductible is met, every covered procedure costs you only your coinsurance percentage (the 20-50% depending on tier). Waiting until January means your deductible resets, so the first few hundred dollars of coverage go toward meeting it again before your insurance starts paying. If you’ve been putting off a crown or root canal treatment, the end of the benefit year is a real and practical reason to schedule sooner.

I’m on Medicare. Does it cover any dental care at all?

Original Medicare (Part A and Part B) does not cover routine dental care, no cleanings, fillings, crowns, or implants. Some Medicare Advantage plans include dental benefits, but what’s covered varies significantly by plan. If you’re enrolled in Medicare Advantage, read the dental section of your plan’s Summary of Benefits carefully. For many adults 65 and older in South King County, a standalone dental plan or out-of-pocket payment is the practical reality for any care beyond what a Medicare Advantage plan includes.

How do I check how much of my annual maximum I’ve already used?

Log into your dental insurance member portal, most major carriers including Delta Dental make this available online. Look for a section labeled “Benefits Used” or “Remaining Maximum” for the current benefit year. You can also call your plan’s member services number (usually on the back of your insurance card) and ask directly. Knowing your remaining balance before scheduling a crown or periodontal work helps you plan whether to move forward now or in the new benefit year.

Can I use FSA money for gum grafting or periodontal treatment?

Yes. FSA and HSA funds can be used for periodontal treatment, gum grafting, and other dental procedures that are classified as medically necessary dental care. These procedures aren’t cosmetic, they address diagnosed conditions, and that means they qualify as eligible expenses under most FSA and HSA plan rules. If you’ve been putting off gum recession treatment and have FSA funds sitting unused, this is worth factoring into your timing.

Have Questions About What Your Plan Actually Covers?

Insurance questions are some of the most common conversations we have with new patients in Renton, and we’d rather answer them clearly before your first visit than let confusion get in the way of care you need. If you’d like to confirm your coverage, ask about treatment costs, or simply get a sense of what to expect, you can reach us at 425-430-0400 or visit cedardentalgroup.com to learn more and request an appointment.